Monte Carlo Simulation Risk

Results Of Monte Carlo Simulation Using Primavera Risk Analysis

Project Risk Analysis Using Monte Carlo Simulation Quantmleap

Risk Management Monte Carlo Simulation Output

Monte Carlo Simulation For Risk At 20 Brazil Download

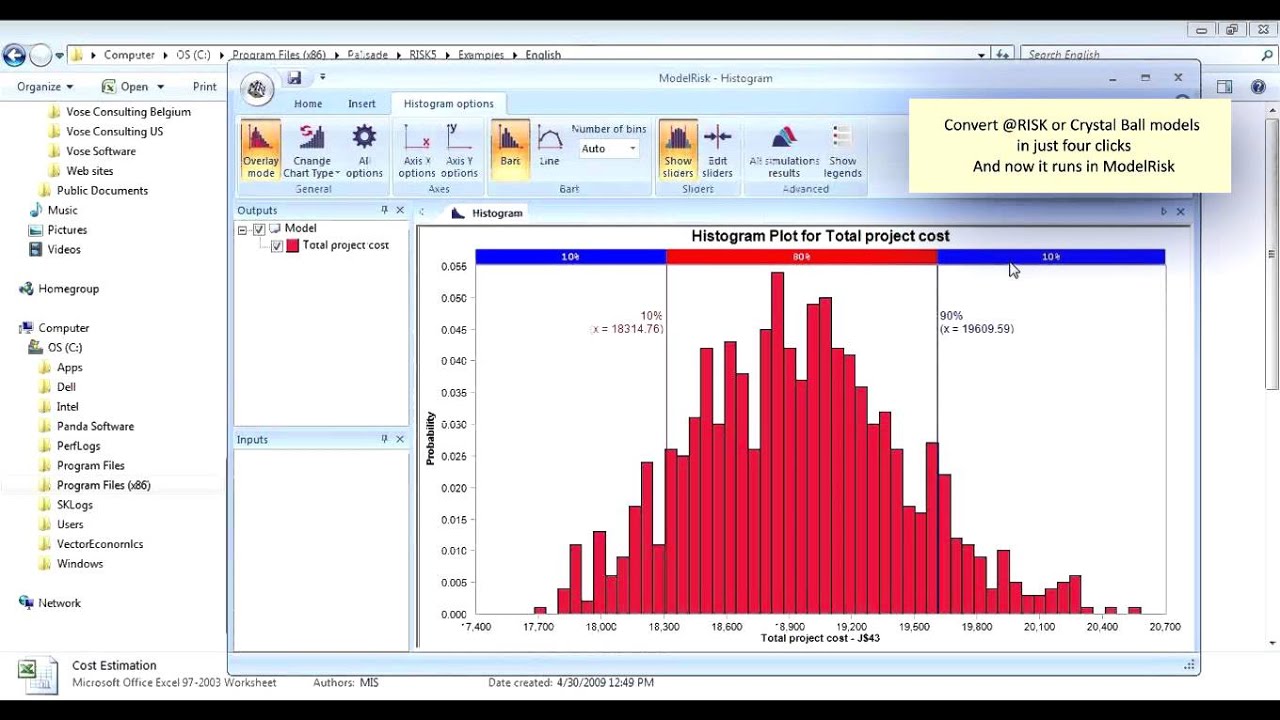

Monte Carlo Risk Analysis In Excel Using Modelrisk Youtube

Https Core Ac Uk Download Pdf 82113269 Pdf

In finance the technique is used in a wide range of applications which include predicting asset prices estimating cashflows pricing exotic derivatives and calculating value at risk var.

Monte carlo simulation risk. Risk pronounced at risk is an add in to microsoft excel that lets you analyze risk using monte carlo simulation. Monte carlo simulation also has important limitations which have restrained epa from accepting it as a preferred risk assessment tool. Available software cannot distinguish between variability. General motors proctor and gamble pfizer bristol myers squibb and eli lilly use simulation to estimate both the average return and the risk factor of new products.

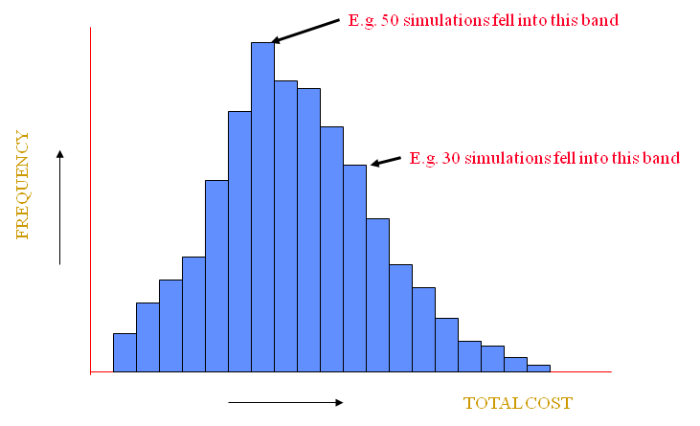

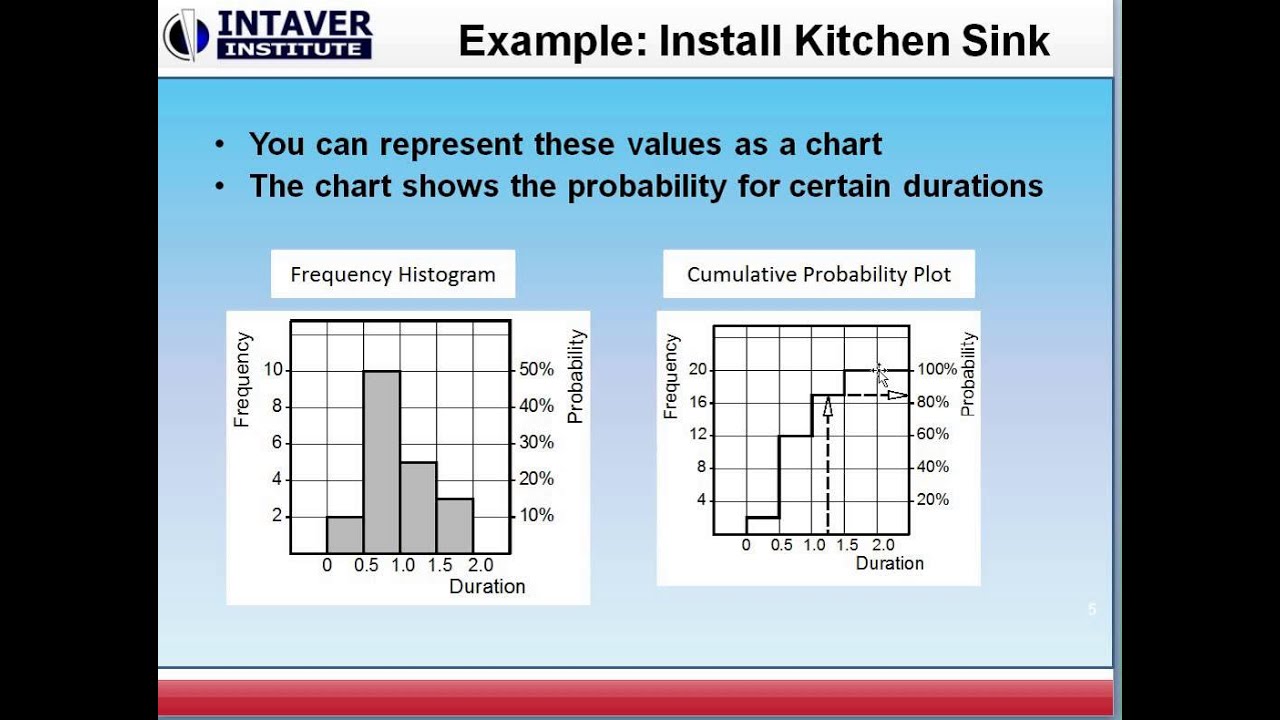

Monte carlo methods in finance are often used to evaluate investments in projects at a. Es wird dabei versucht analytisch nicht oder nur aufwendig lösbare probleme mit hilfe der wahrscheinlichkeitstheorie numerisch zu lösen. Here are some examples. When monte carlo simulation is applied to risk assessment risk appears as a frequency distribution graph similar to the familiar bell shaped curve which non statisticians can understand intuitively.

This means you can judge which risks to take on and which ones to avoid critical insight in today s uncertain world. Monte carlo simulation performs risk analysis by building models of possible results by substituting a range of values a probability distribution for any factor that has inherent uncertainty. Monte carlo simulation allows the business risk analyst to incorporate the total effects of uncertainty in variables like sales volume commodity and labour prices interest and exchange rates as well as the effect of distinct risk events like the cancellation of a contract or the change of a tax law. You get various monte carlo results and graphics as simulation results to analyze in it.

It is a technique used to. Risk shows you virtually all possible outcomes for any situation and tells you how likely they are to occur. Monte carlo simulation is a computational technique used in various scientific applications to model outcomes in a process driven by uncertain factors. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables.

It then calculates results over and over each time using a different set of random values from the probability functions. Depending upon the number of uncertainties and the ranges specified for them a monte carlo simulation could involve thousands or tens of thousands of recalculations before it. Many companies use monte carlo simulation as an important part of their decision making process. Die monte carlo simulation wird häufig für die lösung komplexer aufgaben wie beispielsweise zur messung finanzieller risiken in unternehmen vorgeschlagen.

Die genaue herkunft der bezeichnung für dieses simulationsverfahren ist nicht bekannt jedoch wurde in diesem zusammenhang der begriff monte carlo das erste mal im zweiten weltkrieg als deckname für eine. Als grundlage ist vor allem das gesetz der großen zahlen zu sehen. B risk is a monte carlo simulation software for simulating building fires.

Monte Carlo Simulation Of Risk And Uncertainty In Project Tasks

Result Of The Risk Analysis Based On A Monte Carlo Simulation

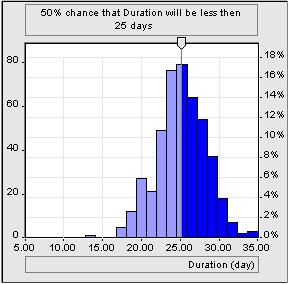

Monte Carlo Schedule Risk Analysis Part 1 Introduction To

Monte Carlo And Manufacturing 2014 04 01 Quality Magazine

Monte Carlo Simulation What Is It And How Does It Work Palisade

Project Risk Analysis And Contingency Analysis Monte Carlo Method

Monte Carlo Simulation Assignment Help By Experts 30 Off

Expect The Unexpected Risk Assessment Using Monte Carlo

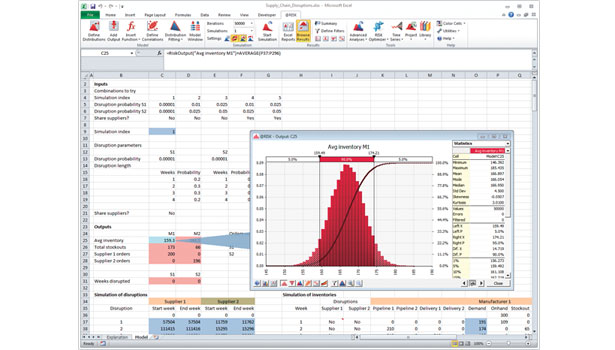

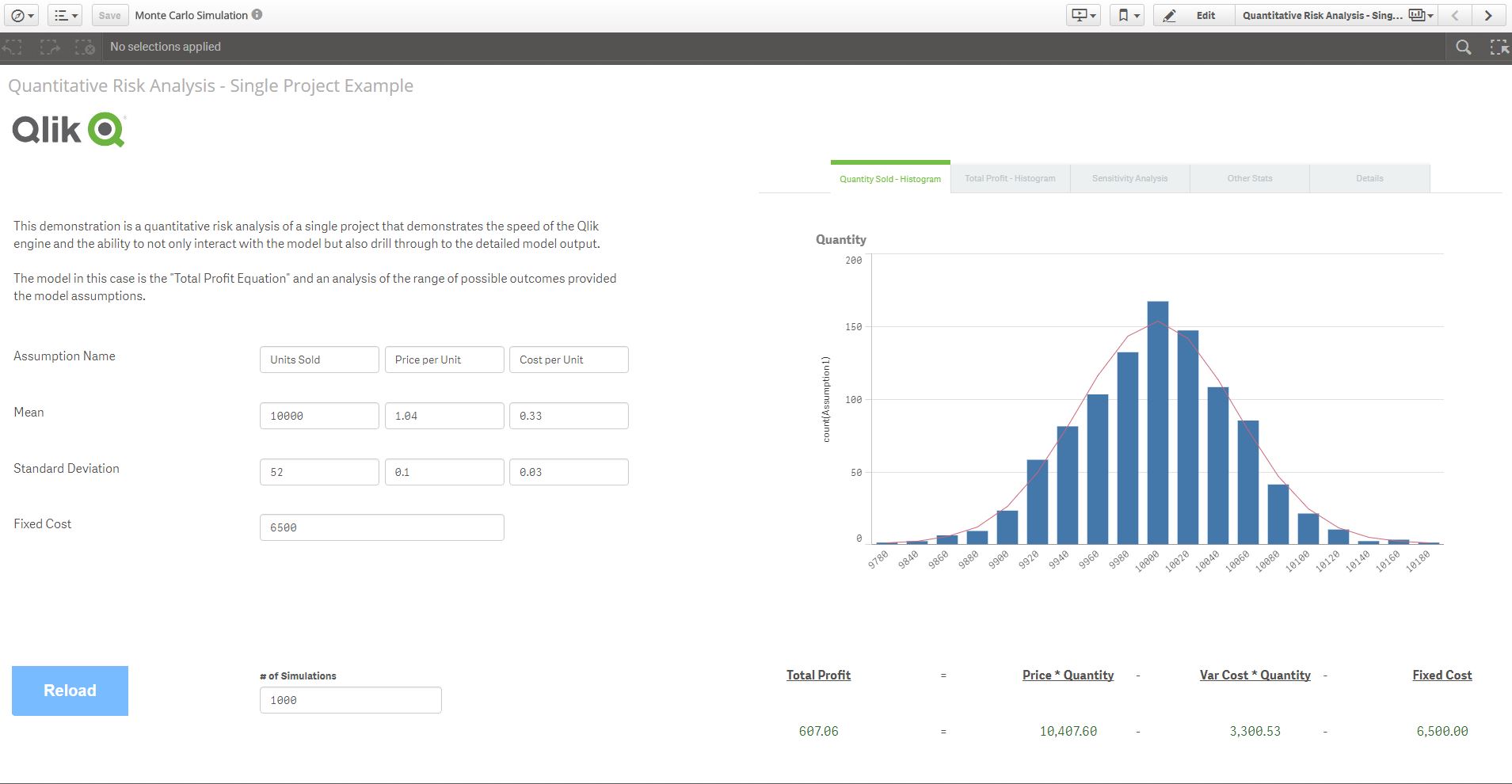

Quantitative Risk Analysis Monte Carlo Simulatio Qlik

Risk Management

Structured Monte Carlo Sap Library Market Risk Analysis

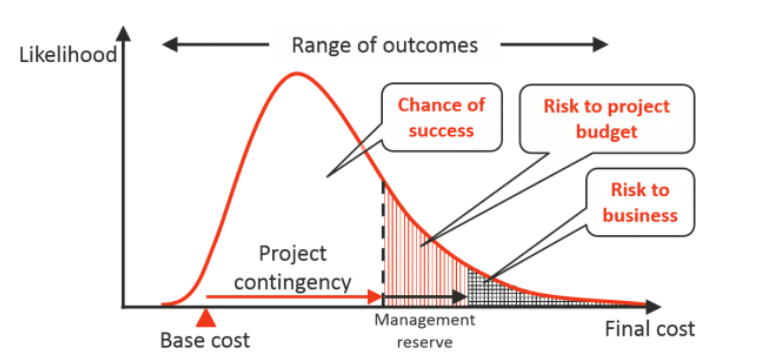

The Surprising Benefits Of Project Risk Analysis

Integrated Cost Schedule Risk Analysis Hulett Associates